Interview with Ben Sandel, Part 2

[Editor's Note: In this section of our interview with Ben Sandel of the CDS Consulting Co-op, Jim Johnson asks how food co-ops can increase their share of the growing organic and local food markets. Sandel suggests re-investment of profits along with a focus on growth, and points to Austin's Wheatsville Cooperative as a notable exemplar. The need for new co-op finacial models, appropriate for urban and lower-income co-ops is also discussed. You can read part one of the interview transcript here. Part three is here This section of the interview starts at 45:34.]

Jim Johnson: Co-ops are growing but still losing market share. And so you have numbers on how fast the natural foods industry in general is growing versus how fast the co-op sector is growing?

Ben Sandel: Those numbers have got to be out there. I don’t have those here, but [...] you look at it [and] you can kind of [...] Your gut can tell you this, that the amount of natural and organics that are showing up in conventional stores, even at Walmart, is growing. The amount of food sensitivities, or maybe our awareness of them, and our attention to them is growing to [...] celiac and lactose and all of the various other [...] challenges out there for people… There’s now more that’s being created for them, and it’s driving people to look for alternatives, which often means naturals, organics, stuff that in the past has generally only been found at co-ops and health food stores. But now you’ve got the Food Lions and the Krogers and the Safeways and the Walmarts who are beginning to carry some of this stuff. I don’t have the numbers on this, but, you know, you look at the last 20 years... Many of the brands that used to be independent brands serving [...] almost exclusively co-ops and natural organics have been purchased by big national brands.

Jim Johnson: Totally. I see that.

Ben Sandel: Which means their distribution also tends to really broaden when that happens.

Jim Johnson: Right. I see that, and yeah, very much. [...] [S]omebody can pay the slot fees and they start showing up in conventional grocery stores.

Ben Sandel: Right, yeah. I think Honest Tea is owned either by Pepsi or Coke [it's Coke -ed.]. I don’t propose which one, but [...] instantly when they’re coming on that truck, well, he’s going to stock them any darn place he pleases in the store, and it’s probably going to be a prominent place. [...] And he’s going to start doing that in any store, not just in [...] natural and organic stores.

Jim Johnson: So there’s a couple different ways to look at growth here, at least a couple different ways. One is stores, and more Whole Foods, or there’s more food co-ops, or there’s more Trader Joe’s or something, ok?

Ben Sandel: Yeah.

Jim Johnson: But another way to look at the growth is conventional stores, existing stores not traditionally natural or organic, stocking more natural and organic products?

Ben Sandel: Absolutely, yeah.

Jim Johnson: And I assume those are the two major ways. Am I missing anything or are those basically the two channels through which the industry’s growing?

Ben Sandel: Yeah. I’m not aware of anything else, but that seems right. And, you know, as an example, I was in my home town of Rochester, New York this summer, which is also the corporate home of Wegmans, which is family owned or family controlled grocery chain that’s now quite large and is also, I think, generally considered to be a very high quality conventional grocery chain. The presentation is very good; their house-branded stuff is very good. It’s just [that] they’re nice stores, you know? No two ways about it. And I was surprised and impressed, frankly, going into a couple of their stores, that they had - all over the store - they had special signage noting organic alternatives they had on the shelves, rather than have [...] like some stores do, there’s our natural section over here, and [...] we’ve got everything kind of ghettoized in one corner of the store.

Jim Johnson: That’s what Giant is doing here now. Yeah.

Ben Sandel: They’re doing the ghettoization or they’re putting it all over?

Jim Johnson: They’re doing the ghettoization, including some stores that had distributed it around, they’ve shifted to a ghettoized model, which surprised me [...]

Ben Sandel: So Wegmans is [...] a lot of their house brands are now organic. And they’re putting it right next to - So you’ll have [...] organic cheerios next to conventional cheerios, but even beyond that they’re putting a sign there that not just says “organic” but says here is why organic is better for you because of fewer pesticides, because it’s better for our environment. And at every checkout they have a sign that says consider purchasing organic instead of conventional in all your future shopping, and giving real reasons for it. So I’m looking at this and being like, you know this is why the market share is growing in conventional corporate grocery. You know they’re probably an outlier in that, I imagine. Certainly we have nothing in our community in the conventional groceries, anything like it. But I imagine they’re doing this in all their stores throughout their organization, and so they’re definitely building awareness and a much larger audience that “Oh yeah, maybe I should think about that.” Or, you know, if my kid has been getting sick all the time maybe food could be a reason [and] an area that I could improve his life or her life.

Jim Johnson: Well, and clearly Wegmans sees this as a strategic opportunity.

Ben Sandel: Absolutely.

Jim Johnson: A big one. A big one. This isn’t just, “Oh, we got to do this because everyone else is doing it.” They’re leading with it, or they’re trying to.

Ben Sandel: Yeah, it’s a strong differentiator against their competitors, and you know conventional grocery grows - the sales growth is pretty much the rate of population growth, whereas as natural and organics are growing much faster than that. And so, yeah, they’re definitely seeing this as a major differentiator, something they can point to. And I think they’re also seeing it as something that - and this is an area that I think co-ops should totally pay attention to because of the quality of their organization - they can do this better than many of their competitors, and I think co-ops also can do it better.

Jim Johnson: Quality of organizations... You mean, really, quality of management, tightness of operations?

Ben Sandel: Management, ordering, merchandising... You know, I mean just like what I described as to the extent they’re going in their merchandising. Co-ops can do the same thing [...] And I think Wegmans also values their relationship with their consumers, their shoppers, and cultivates it so that when they present this information, their consumers are a little more likely to trust it than they might if they went to their Food Lion and saw the same thing.

Jim Johnson: So co-ops are growing but still losing market share. Is Wegmans and conventional grocers starting to carry some natural and organic - does that really threaten food co-ops? Could it be “the rising tide raises all boats” and people get turned onto natural and organic, and they might eventually end up becoming more attracted to a one-stop natural and organic place? No?

Ben Sandel: Well, I would say it’s in between that. I think there’s a real opportunity there and [...] I think the threat exists if food co-ops don’t do anything about it, if they continue to do business as they’ve always done or as they’ve traditionally done, then yeah there’s an absolute threat out there because one of the things that - and this is now where I guess I’d say this is veering into my experience and opinion not necessarily backed up by - you know, but anyways, enough provisos.

You know Wegmans has substantial financial capabilities that they are putting directly into new store growth and improving their existing stores. So they’re using these funds in that way. Food co-ops have often been reluctant, and now I’m talking less about new stores from scratch, new co-ops, [...] but more of existing cooperatives expanding and growing. They’ve tended to sit on their equity. You know, it’s their members’ money and they’re concerned about it, which in some ways that makes sense and is a valuable perspective.

Jim Johnson: But they don’t keep reinvesting.

Ben Sandel: But they don’t keep reinvesting. So if they continue in that way, I think that [...] could be a major threat, that sitting on this money means that eventually they’ll earn less and they’ll start using up their equity until their market share shrinks, until eventually they’re out of money and they begin to lose money and they go out of business. So on the other hand, if they look at this rising tide which I think does [incomprehensible] and say “awesome,” you know [...] we’ve been shouting this message for decades and now it’s being heard. Let’s double the size of our store and open three new ones because now we have demand to support it. And because they’re always [...] compared to our three-decade-ago store, now we are a first rate retailer who can compete head to head against anybody else who comes into our market. Which, I mean, [...] frankly not many of those stores 30 years ago could have done that, you know, head to head. They didn’t have the same station; they didn’t have the staff capabilities, you know.

Jim Johnson: Correct me if I’m wrong... They survived only because they were monopolies essentially.

Ben Sandel: Yeah, and because they [...] had a certain caché that some people were [...] willing to put up with [...] because you had the caché, you know. It’s cool.

Jim Johnson: Or that some people like. [laughter]

Ben Sandel: Yeah, or that some people like. Yet it was restrictive to reaching a much wider audience.

Jim Johnson: Right. And so is it fair to characterize the old way, the sitting on equity approach, as complacent?

Ben Sandel: Yeah, I think that’s a word you could use. “Cautious” might be a nicer word.

Jim Johnson: Right. Cautiousness that maybe becomes complacency because reinvestment takes risk.

Ben Sandel: Right.

Jim Johnson: Right?

Ben Sandel: Or it turns into overly-cautious, yes. It does [incomprehensible] to go take risk. But on the other hand, there’s a great, even greater risk, I think, in doing nothing.

Jim Johnson: Well... And so, if we’re still losing market share do we- Here’s the devil’s advocacy question.

Ben Sandel: Yeah?

Jim Johnson: Can we really say that our current model, if we want to call it that, what we [...] might call it the dominant model - I think there’s only one model that we can say seems to be- There seems to be only one model that NCGA feels comfortable with and it’s [...] the CDS model, essentially, right? Correct me if I’m wrong.

Jim Johnson: Can we really say that our current model, if we want to call it that, what we [...] might call it the dominant model - I think there’s only one model that we can say seems to be- There seems to be only one model that NCGA feels comfortable with and it’s [...] the CDS model, essentially, right? Correct me if I’m wrong.

Ben Sandel: Well, I mean that’s the one model that so far appears to work over and over again. I wouldn’t say it’s the only one they’re comfortable with. It’s the one that they’re using now because it has been proven over and over again. I think everyone, including NCGA, is looking out there to see what might work with different circumstances, different sizes, et cetera. We just haven’t really come upon that yet, but everybody is looking for this.

Jim Johnson: That’s good. That’s what I wanted to hear, and that’s something that I think a lot of people are not aware of. You know, that they might not even conceive of the fact that there is this one model and there’s a sort of a general consensus amongst the seasoned food co-op people that this is by far the most proven model.

Ben Sandel: Well sure.

Jim Johnson: But-

Ben Sandel: I mean, it is the most proven model.

Jim Johnson: The safest model? What’s that again?

Ben Sandel: It is the most proven. It is the safest, but also I think we all were faced with this situation where [...] co-op growth had been very slow for a very long time, so nobody really [...] You know, Stuart Reid and a bunch of others, when [...] the original thinking behind Food Co-op 500 was we had to get- we’ve gotta jump-start the movement, and which has worked. All of a sudden there’s this really incredible upswell in activity in starting new co-ops, and I think everyone now has been trying to... I mean, we are still a small industry so there’s not a ton of overhead that can be instantly shifted to let’s start working on this. So [...] there is a little bit of a lag time. [...]

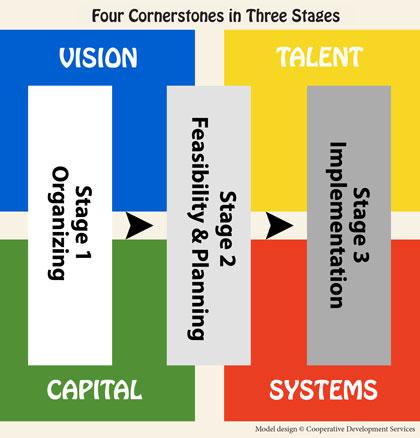

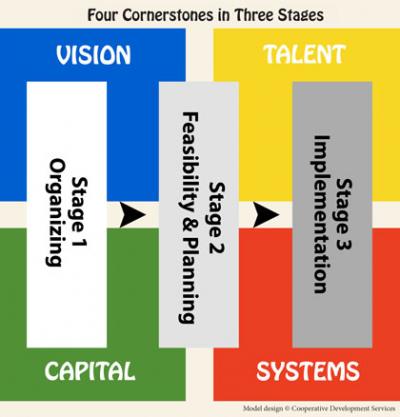

You’ve got people like Bill Gessner who’s part of CDSCC who was really- he is the person who created the four cornerstones in three stages model based on [...] 35 years of experience with new and expanding co-ops and with helping co-ops kind of move into a new era of professionalism and service. So [...] we know that that works pretty darn well and is reproducible. But I think everyone is open to the idea of there’s probably other ways, too, but it’s hard to- [...]

Walmart, for instance, is experimenting with different size stores all over the country - various sizes - because they have the capabilities, financial capabilities that they can open 20 stores of varying sizes, assess the performance, and then close the ones that don’t work. The [food co-op] industry doesn’t have the resources to do that. So that’s why we would love to see some of these models out there, but there is a bit of a chicken and egg challenge here that-

Jim Johnson: Yeah, very much.

Ben Sandel: We need to see it work before we’re going to put resources into it; we need to put resources into it before we can see it work.

Jim Johnson: And that’s sort of the devil’s advocacy question that I have. It’s like, “Ok, we’re growing, but we’re still losing market share.” [...] [A]nd we have this sort of prevailing model, and yet it sounds like folks are aware we can’t say our prevailing model is enough as long as we continue to lose market share. I’m looking at what is it we need to be doing, [...] and it’s not just the model question but in the area of models in order to do what we need to do, i.e. stop losing market share, hopefully get to the point where we’re gaining market share, ok? What do we have to do to get there in terms of models? And I’m asking you to speculate broadly here.

Ben Sandel: Yeah, but I don’t entirely agree that [...] we’re at that place now, because I think we’re still very low in the growth curve, and, especially with existing co-ops, I think there is a huge amount of potential with existing co-ops growing much more quickly than they have in the past. And some of them are embracing that and are even trying to sort of codify it so that other co-ops can follow their lead.

Ben Sandel: Yeah, but I don’t entirely agree that [...] we’re at that place now, because I think we’re still very low in the growth curve, and, especially with existing co-ops, I think there is a huge amount of potential with existing co-ops growing much more quickly than they have in the past. And some of them are embracing that and are even trying to sort of codify it so that other co-ops can follow their lead.

So like Wheatsville in Austin, Texas, they created their BIG program, “Business Is Good.” That’s all oriented around "here’s our mission, here’s our vision, our global end, and if we want to do it for more and more people and eventually kind of turn this into the largest- you know, serving the largest number of people possible and improving our world the most we can, the best way we can do that is continue to grow." And that, you know, it’s a change in thinking, and they’re putting a lot of resources [in].

They renovated their first store, which is their only store for the moment, and substantially increased its size and the business immediately followed, so that was a huge financial success. Now they’re in the process of building their second store in a different part of town and they’re using the same model. You know, they’re doing the same thing of putting the cornerstones in place, going through the stages. It works for new co-op startups and for expansions or new stores for existing co-ops. And I think, if anything, that model works [...] really well for startups and for existing co-ops, so that we are still losing market share is not so much that we still need more models, yes we do, but it’s more that we’ve not begun to see successful co-ops really flex their muscles. [...]

Jim Johnson: That’s interesting. So you think that our prevailing model does not have shortcomings. So we’re still realizing it's potential-

Ben Sandel: No, every model has shortcomings [...]

Jim Johnson: I’m overstating that.

Ben Sandel: Yeah.

Jim Johnson: It’s still realizing its potential. You say we’re still at the beginning at realizing the potential of this prevailing model?

Ben Sandel: [...] Absolutely not yet realized the full potential there.

Would I love to see another model that works in a more urban setting? Yes. And I want to make sure there’s a clear distinction. I think the four cornerstones and stages model will work in any cooperative. It’s a basic developmental tool that makes sure that you- all the steps you need to to have a successful startup regardless of what size. The model aspect that is the challenge is the financial models that we’re currently working with that’s very, very hard to scale down below a certain size or a certain amount of sales. [These financial models recommend $50,000-$150,000/year median local incomes and over $2 million in yearly sales in order for a food co-op to be viable, as discussed in part one of the interview. -ed]

And, you know, [...] that’s kind of the allusive “other model” is can you do a store with substantially less refrigeration? Well, you know, obviously that affects what you’re going to carry in the store. And will it be profitable? That’s the questions that, [...] in my opinion, is still the open question. And you know it may be, then again, [...] you look at [...] what we would consider a large food co-op is a very small conventional grocery store. So what we’re seeing as a small food co-op, conventional grocery stores would not even begin to look at. You know they’re [not] going to look at a 2,500 square foot store. It has no attraction to them whatsoever because they look at that and say “massive money loser forever.” But yet we’ve got a lot of people in the co-op world who want to open stores at that size.

Jim Johnson: Yes.

Ben Sandel: And, you know, although it is very possible that a number of those people want to open them that size simply because they don’t know that that’s, [...] so far by all accounts, that’s not a viable size. You know, they’re not aware of that yet. They haven’t gotten down the path far enough to realize that. And my experience with startup groups is, especially in the very early stages, they dramatically underestimate the resources needed to open a co-op. They can’t- they don’t know. You don’t know what you don’t know.

So, you know, you think, “Oh, we’ll buy some used equipment for $60,000 [or] $70,000; we’ll get everything we need to start up the store and we’re good to go.” Well, you know, your point of sales system’s going to cost you $60,000. So [...] where does that leave you? [...] [Y]our cheese display case is going to [be] [...] $14,000 on its own. [...] [S]o all these things start adding up real quickly. And of course, also there’s, “Well, we’ll just buy all [...] used stuff at auction.” And then you get it and realize that [...] the seals have cracked because they weren’t stored properly, and all the copper fittings, including your refrigeration tubing, has been stolen because copper was [...] still valuable. And all these other things that you can’t- you don’t know. So it’s hard.

You know, if somebody could create and UNFI does this to some degree. You know, they will help connect a co-op with reputable refrigeration companies that will sell refurbished products. But they make a real distinction between not used [and] refurbished. [...] Don’t go out and pick Craigslist and buy yourself a used cooler, but if you buy it from reputable [...]

Jim Johnson: You need to buy something that’s been tested and is known to work, et cetera.

Ben Sandel: Yeah, because it’s not [...] just your initial startup costs that come into play in those decisions. It’s also how does that work with customer retention and customer service? When somebody says, you know, “My kid’s birthday party is this afternoon, and I’m here to get the soy ice cream because they can’t have regular ice cream,” then, oh, your freezer went out last night. You don’t have any. That is a bad situation.

Jim Johnson: I hear that. And the equipment thing is misleading for a lot of people that don’t realize the maintenance. And particularly when you’re buying, like you said, they don’t know what they don’t know. They don’t know how difficult it is to buy used, any kind of used equipment, you know, as is. You really [...] could be getting something that’s pretty much worthless.

Ben Sandel: Right. And those expensive fixtures are [...] at the four walls of the store, so if you make your store smaller, you’re still buying freezers and coolers. They don’t know a cooler half the size isn’t half the cost, so that’s one of the problems with scaling down to a small store is your [...] cost per square foot actually goes up and, for that matter, your labor per square foot goes up, too, because [...] if you have a 6,000 square foot store and a 3,000 square foot store, you don’t pay your general manager half the amount, you know. [...] It’s kind of where the lie of like a flat tax; it’s the same [...] false logic.

Go to Expanding The Reach of Food Cooperatives theme page

Go to the GEO front page

Add new comment