Imagine that you agree to join a cooperative, but when presented with the membership agreement, you find that it is written in a language that you can’t read. When you ask for a version in English, you are given a summary of what the contract says, but not a direct word-for-word translation; and when it comes time to put pen to paper, you are required to sign the contract that’s written in a language you don’t understand. Would you go ahead and sign up for that co-op anyway? Would you pay for a membership and agree to the terms of the bylaws, despite not being able to confirm for yourself what’s in them?

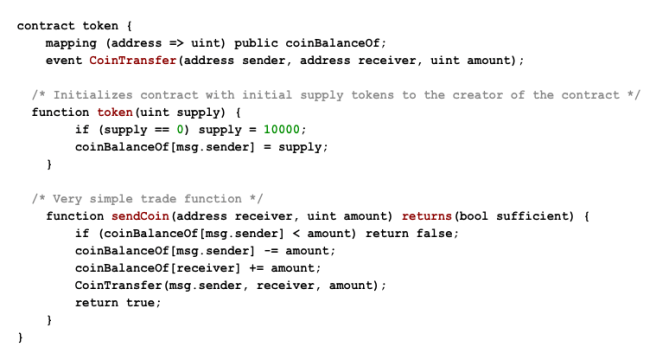

Blockchain technology has many serious flaws, such as its atrocious carbon footprint, that have been covered extensively elsewhere, so I’ll not bother with them here1. But what I haven’t seen discussed is this fundamental flaw, this Achilles's heel for cooperative projects on the blockchain – and specifically for DAOs (Distributed Autonomous Organizations), which are the particular aspect of cypto that cooperative-inclined people have been leaning towards as of late. The promise is that through the use of “smart contracts,” organizations can be created “on-chain” that allow people to make collective decisions – usually about the use of funds collected from those same members. And that does sound kind of co-opy on the surface, but the problem with this concept is that an actual smart contract looks like this:

And that’s an extremely simple one. An actual DAO smart contract could easily be a couple pages of such code.

To be fair, it is true that co-op bylaws can contain a bit of legalese that sometimes takes a bit to parse, but at least to read a set of bylaws, give meaningful feedback on them, make suggestions for changes, or give your informed consent to them, you don’t need to learn to code. But when it comes to DAOs, that’s exactly what you need to do. If you can’t understand the code the contract is written in, you are put at the mercy of those who can, and you have to take their word for it that the contract says what they tell you it does. You have to trust that there isn’t a line of code in the contract somewhere that allows someone to, for instance, transfer group funds to an anonymous wallet, thereby robbing the members. Unsurprisingly, that is exactly what has happened with DAOs over and over again2.

This problem is fundamental to the design of DAOs: 1) most of the participants will not be able to understand what smart contracts actually say, and 2) the actions of those smart contracts are – by design – automatic and irreversible3. These two facts combine to create a situation in which most DAO members are placed in a position of having to trust whoever coded the contract, with no way of holding anyone accountable should that trust be violated. This is obviously a highly problematic way to try to build a co-op...to put it mildly.

And while this issue of having coordinating documents written in a language most people don’t comprehend is likely a fatal one, there are several other serious problems with the idea of DAOs as a useful addition to the co-op toolkit. The major one is that, despite having been around for several years at this point, no one seems to be able to point to any real-world, beneficial project that they’ve been used for. The only use case for DAOs appears to be moving crypto tokens and NFTs around on the blockchain. I put out a request for examples of DAOs doing something useful in real life on social.coop, and even tagged a few people and groups who would be in a position to know about any. The only thing I got in response were papers about “the potential of DAOs” to do something useful. But the potential of DAOs has been being touted for years now, with nary a sign of that potential amounting to anything real “off-chain.” Stories of projects abandoning their blockchain aspects after figuring out that they were unnecessary abound, but stories of the blockchain actually being essential (or even useful) appear to be non-existent.

And while we wait for the potential of DAOs to become anything more than idle academic musings, more and more people get sucked into the crypto ecosystem by the hype, kept in the dark about its manifold problems, and often enough end up getting their pockets (or rather, their wallets) picked.

The reality is that DAOs, and the entirety of the cryptosphere, is a solution in search of a problem. It has been hyped up as cutting-edge and therefore has attracted the interest of people who are generally interested in cutting-edge tech. Unfortunately, the tech has proved to be mostly useless for much of anything apart from providing a platform for ponzi schemes, and enabling money-laundering (which, to be frank, is why I think bitcoin was created in the first place). Of course, that’s not much of a recruitment pitch, so the enthusiasts have had to come up other justifications for the existence of these crypto tokens over the years – their supposed usefulness for social projects is but the most recent of these.

First crypto-currencies like Bitcoin and Ethereum were pitched as alternative currencies that would free the people of the world from state-controlled money. But it became clear pretty quickly that they were unsuitable for that purpose, given the wild fluctuations in price caused by the fact that most people were buying them as a long-shot investment, not because they wanted or needed an alternative to VISA.

So next, crypto-backers leaned heavily into the investment angle, seamlessly transitioning from marketing their tokens as a way to escape state-controlled money, to pitching them as a way to obtain a bunch of that state-controlled money – culminating in 2022’s Super Bowl commercials being dominated by ads featuring celebrities extolling the virtues of “investing” in crypto...famously, right before the entire crypto market tanked.

The angle now being pushed by those who, for whatever reason, feel compelled to try find some use for this “technology” is building co-ops — or at least things that kinda-sorta resemble them4. But here’s the thing: we can already create co-ops to do anything we can think of. We don’t need crypto tokens to allow us to make decisions together, and we don’t need inscrutable smart contracts to carry out those decisions. We don’t need the blockchain, or any other hyped-up technology, to build a cooperative commonwealth.

We need to get better at democratic discussion and decision-making; we need to get over our materialist-individualist mindsets that cripple our social imaginations; we need to take lessons from people like the members of Cecosesola, who have provided untold amounts of real world goods and services to their members, for decades, without any need for technocratic solutions, using only the resources available to a Venezuelan barrio.

All of which is to say what we need is more solidarity, not more gee-whiz technology, and you’re not going to find that on the blockchain.

- 1Though those interested in a technical explanation of those many problems are encouraged to read this talk that computer scientist David Rosenthal gave to a Stanford EE380 class https://blog.dshr.org/2022/02/ee380-talk.html

- 2https://web3isgoinggreat.com/?tech=dao

- 3Although, as it turns out, not all smart contracts may be as immutable as advertised, as some projects now use “upgradable” contracts. Of course, that just raises the troubling questions of who can change the contracts and how – questions that will not be addressed here, as there’s plenty of other, bigger, problems with the whole crypto “ecosystem”.

- 4And while most of these co-op crypto-backers are acting in good faith, and actually want to build socially beneficial projects, there are also more nefarious forces at work, who are trying to figure out how to use the special status of cooperative shares as a way for crypto investors to avoid securities regulations. So while crypto-cooperators may think that they are going to be able to use the blockchain for their own purposes, it seems far more likely that blockchain investors (i.e. wealthy individuals and financial companies) will be the ones using co-ops for their own ends. See https://tax.kpmg.us/content/dam/tax/en/pdfs/2023/cooperatives-path-to-compliance-web3.pdf

Comments

ilo

August 24, 2023, 3:34 pm

I liked reading this article because it points out a lot of flaws plaguing online permission-less communities.

I agree that most of crypto activities to date have been about speculation and value extraction by large players.

However, I fear the author is blinded by his own predispositions.

In a world where state-controlled money is out of bounds (inflation disproportionally affecting the poor, bank accounts shut down for political reasons, etc.), bitcoin does provide a safe haven and alternative path, one that is gaining increasing adoption in inflation-ridden countries such as Argentina and Turkey despite it's volatile USD price. In addition, the argument that the technology is bad for global warming is losing steam, with even the ESG movement now understanding the nuances and starting to embrace the technology.

This does not address the point of this article, which is about smart contracts, but I disagree with throwing the baby out with the bathwater. Cryptography has value, p2p networks have value, censorship-resistant means of transaction have value. There are many non-exploitative usecases for these, such as Ricardian contracts, eCash protocols, the Nostr protocol, etc.

ViolentlyTasty

November 24, 2024, 5:03 am

I agree with your sentiment about not understanding the code and having to trust the programmer. I also understand that blockchains are not perfect. However there is an "old guard" in the farming coop world and a complete lack of a more diverse horticultural coop (at least in my region). This old guard likes their way of doing things in an industry based around government subsidies and heavy bank involvement, two entities I do not trust. The utility and community governance of blockchain tokens/apps is allowing me to build this and give access to many people that the farmers coop in my area would charge full price. and to boot, learning to understand the code is easier for many younger people than learning legalese.

Add new comment