An Interview with Christina Jennings

Executive Director of Shared Capital Cooperative, Christina Jennings, discusses how Shared Capital operates and how they have been acting to serve their members and the wider cooperative community during the COVID-19 pandemic.

Transcript

Michael Johnson: Hi, I'm Michael Johnson, and I'm with Grassroots Economic Organizing. And in this interview, we're going to be talking with Christina Jennings, the executive director of Shared Capital Cooperative. And Shared Capital Cooperative is an organization that connects cooperatives with capital. And I'm not gonna go any further with any description. I'll, let Christina do that job and I'll just ask her some interesting questions. Hi, Christina. How are you today?

Christina Jennings: Hi, Michael. Nice to talk to you.

MJ: OK. So just give us a kind of a brief overview of what Shared Capital is and then what you all do.

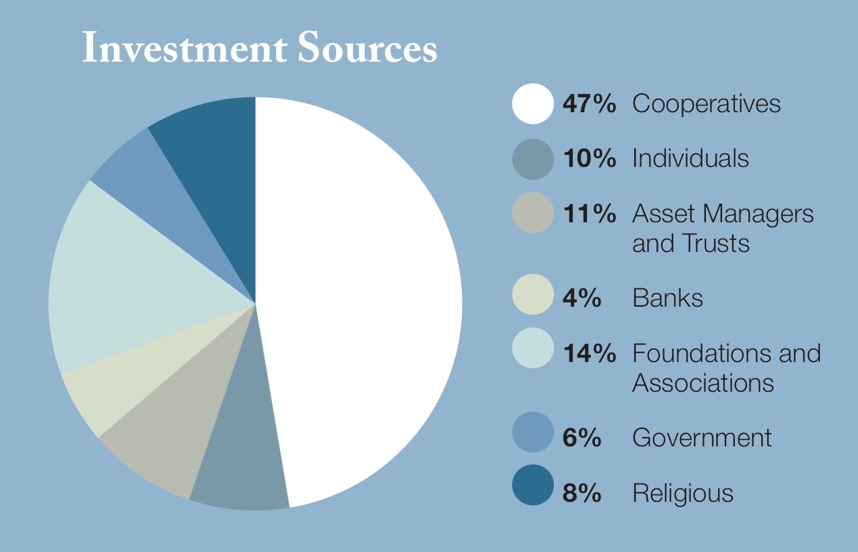

CJ: Sure. Share capital is a cooperative of co-ops, so we're a cooperative owned by cooperatives. We've got about 250 cooperative members who invest in --

MJ: Excuse me, 250?

CJ: Yeah. 250 cooperatives from very small to a little bit larger across the country. And they're investing in shared capital, putting capital into our fund, and also borrowing from Shared Capital. So we're a loan fund. And I'll throw out terminology for those who care about it, but we are a Community Development Financial Institution, or CDFI, and a loan fund that provides financing just to co-ops. And again, we are owned by the cooperatives who borrow and invest in us.

MJ: So when you say co-ops, you are talking about housing, worker, producing, etc. food co-ops, the whole nine yards.

CJ: That's right. We are cross-sector - a cross-sector of co-ops. We work in housing co-ops. We work with small farmer producer co-ops, we work with worker co-ops, food and other consumer co-ops, and purchasing co-ops. So yeah, across that across the gamut, any type of cooperative, as long as they are operating on a cooperative basis, can be a member and borrow from or invest in the fund.

MJ: How did you end up in this business, this industry and at Shared Capital.

CJ: I came out of student organizing and a variety of types of economic and social justice organizing. And I realized that access to capital was pretty powerful, -- those who have it could do a lot more that those who don't. So I trying to find ways of moving capital into the various movement work I was committed to. That started with fundraising and grant access, but what I realized was that had some limitations and so started looking at different types of investing, social impact investing it was called, and now impact investing. And so I ended up getting involved in first working with some loan funds that worked with small businesses and communities, trying to provide capital to folks who didn't typically get access to the capital. And really frankly discovered co-ops along the way in that work. That's when I really learned more about co-ops. I was working with all different kinds of small businesses, local businesses, and realized that co-ops: I loved the model, didn't know it all that well, got to know it a little bit better. As I encountered more co-ops, I became more excited about them, about the possibilities of the collective work toward shared goals, rather than throwing every individual to the whim of the market and hoping that they fend for themselves. Realizing that if we came together and really worked on these issues, we could really make more of a difference. And so, I was really excited to get involved with Shared Capital. About twelve years ago, I came on board. We'd been facing some tough economic times as part of the Great Recession, and I came in to try and work with the existing board and staff to sort of find our path going forward out of that. And so I've been with the organization since then.

MJ: OK. So has the pandemic affected your organization and access to capital, etc.? If you could just kind of tell us about that.

CJ: Yeah. The pandemic has affected our access to capital in a couple of ways. One is that when we started being aware, just as things were unfolding, I guess, we saw that a lot of people were really anxious about the economic situation. And so we immediately offered to all of our borrowers the opportunity to just defer payments for a period of time while we all figure out how this was going to impact us.

And so that was really important to do, but it also meant we had a lot less capital coming in. Usually we've got money coming every month from our borrowers that we then can put out as new loans. In addition to going out and raising new dollars we're putting that money that's coming back in to work. So that had an immediate impact. It was really important to be able to do that, and I'm pleased we are able to do that, but it does reduce the funds we have available for new loans.

And then in addition to that, we did see some funders -- we were in the middle of applying for one investment -- it would have been a large loan to us or a grant to us depending on how it played out. And that large funder announced they were not going forward with their plans because they needed to shift their focus. So that was disappointing.

Fortunately, we've seen some other really committed investors and funders who said, "oh, now more than ever, we need to make sure we get money out, and we get it out efficiently and quickly so that folks can put it to work where it's needed." So we've been turning to those funders, and away from those who are shutting down the channels.

MJ: OK, so I noticed on your website that you you are in a position to provide emergency loans. Is that still the case?

CJ: Yeah. So, in addition to allowing our existing borrowers to put off payments for a period time so that they can hold their cash while they need it, we also are offering emergency loans to those who need additional cash. Both our existing members and borrowers, as well as other co-ops. So we have made a number of small emergency loans just to help folks cash flow through this time, having the cash to pay the most critical things. We're also trying to work with those co-ops to help them figure out how to how to make adjustments so that they can survive, as well as access the various Small Business Administration emergency funds. So, yeah, but we have our own small pool of emergency funds.

I'll just say our board was really responsive and they stepped up. They tried to make it available more quickly than our usual process. They made a simplified application. We made a simplified approval process so we could try to get dollars out quickly. The maximum is $50,000, so it's not a lot of money. And we realize that debt might not be the solution, for everyone during this time. But trying to get dollars in the hand, then have a pretty flexible repayment plan for those who borrow.

MJ: And anyone that's watching that is interested in exploring that possibility, they could just contact you through your website.

CJ: That's right. They can email info@sharedcapital.coop or go to our website, sharedcapital.coop and get more information.

MJ: OK. So let's turn and talk a little bit from a movement prespective. So, loan funds are a very critical part of the co-operative movement. And so you're one part one piece of that part. What do you know about how the pandemic has impacted the whole field of co-op loan funding, or if there's a more appropriate term than that?

CJ: No, that's great. That's good terminology. There are a small group of of loan funds that primarily are serving cooperatives. We're part of a larger field of small business and housing loan funds that don't that don't necessarily work with co-ops. And so we've been and we've been actively in touch with other co-op loan funds. And I think what we're hearing is -- we we were sort of comparing notes last week. So what I've heard is we're all experiencing about a third, 30 to 40 percent maybe, of our borrowers are unable to make payments right now.

MJ: Wow, that's a big number.

CJ: Yeah. Hopefully, many of them are position so that once things start to reopen and carry up and safely, they'll be able to start working again.

So that seemed to be -- it was interesting how uniform that was across our experiences, when we are comparing notes. And then we're all trying to figure out how to make sure that the co-ops that we're working with can survive this time. I mean, it really comes down to that for many of them. The doors are closed. They may not be operating at all, or they're operating under really tough conditions because of the pandemic. And so, I think we're trying to make sure that they can continue to take care of their workers, take care of their members, whatever type of co-op they are, and then just get through this so that they have the chance to reopen and be successful after this.

MJ: One question that I really don't know the answer to. I did preparation but this question I didn't come up with until just now. Owners of worker cooperatives are not in a position to apply for unemployment benefits. So if a worker co-op business has to close, they can't tap into that source of income. Is that correct?

CJ: Well, it depends somewhat on the structure of their work co-op, so we have some work co-ops where the workers are technically employees and therefore can apply for unemployment. And then there also are some -- if they're members of an LLC or if there are some provisions under some unemployment, I don't know all of the details. I don't claim to be an expert, but I know that there are some opportunities for LLC members. The catch is, also, if folks aren't legal residents, or don't have a green card to work, they're undocumented, then that can create some real hardships for those workers. And that's been an area that we've been spending some time on. And then for other structures it can be complicated.

So, there are complexities to it. And frankly, just figuring out what you can and can't apply for has been a challenge for folks. And then, even if they figure it out and they apply, sometimes they're just not hearing back about this program.

MJ: I'm a member of an intentional community in New York City. And we had to close two our two primary businesses. We had to close two of the businesses because they're not essential. But the community itself is a business. It operates like a business. So, the workers from the two retail businesses have been able to apply for unemployment. And the community depends upon their dues to the community as operating capital. And so that has made us going forward -- well, it's very helpful. And we've also been able to apply for that small business loan. So that's one way in which we've navigated these waters also.

CJ: That's a great example. You gotta be creative.

MJ: It's a very challenging time for sure. Do you have any sense of where things are headed, where are we going with this? Or are you kind of like, "oh my God," you know, like everybody else.

CJ: Oh, yeah, we definitely don't have any magic insights. Unfortunately, we're operating with the same information others have, with the advantage that we get to interact with a lot of different co-ops around the country. So we get lots of pieces of information, I suppose, but we don't have any great insights into the future.

I think, right now what we're seeing is that are our co-ops, that we're working with, co-ops, that we are seeing around us, many are just on hold. Some are starting to reopen or planning for reopening. Actually we work with a fair number of food co-ops and those folks have been working really hard through this. They've been really stepping up to try and make sure that food is available in their communities and that they can offer an array of services, whether that's delivery or curbside pickup.

We work with other essential businesses like home care co-ops that are continuing to have to find ways to operate during this time. In some ways the pandemic has created so much uncertainty, but I feel like right now the big question that we're asking is what kind of economic recession are we going to see and how long is that going to last? And we have no unique insights other than we know that there will be a significant impact even once the economy starts to reopen. And it feels like almost that's the place where the greatest uncertainty sits for folks. Because if things could reopen in a couple of months, and folks could restart their businesses, many of them could get by, because co-ops are awfully resourceful and creative and resilient. But if folks don't have money, if the community have money to buy the products or services they're selling -- well, who knows? And that's going to create even more distress for them.

MJ: The whole factor of demand seems to be the one thing that a lot of the people that are pushing for reopening aren't taking into consideration, because if people aren't going to go out and buy then there isn't going to be the demand to really support reopening.

CJ: Yeah, if you're not working right now, you've got limited or no income coming in. Maybe you've tapped unemployment, but maybe you haven't. I know lots of folks who've tried and maybe haven't been able to get through those systems. So, I sense that's a huge factor. There'll be both the fear of what will be -- there'll be the fear for some of our co-ops that are working very closely with people. Will people want those services? How quickly will they want folks back in the home, but also, will they even have money to buy them?

MJ: So I want to ask one final question, of course, this is the one that is probably the most challenging. Worker cooperatives are part of the whole small business world. And I run across a lot of speculation that small businesses are going to be maybe out of business. The whole way in which the economy is going to restructure, etc., etc. You just aren't going to have that much space for small businesses except online or what have you. Not expecting any wisdom or great insight, but just what you might have to say about that. To whatever extent you can.

CJ: Well, I suppose I couldn't do this work if I wasn't a bit of an optimist. So I have to say what I think. We've been working with startup workups, expanding worker co-ops, and now quite a lot of businesses that are converting to worker ownership. And I see -- one, I see an enormous amount of resilience. I mean, you don't want resilience on the back of people trying to support their families. But there is a lot of ability among worker co-ops to find ways to get through tough times. We've seen that. And we think that's still true. We still certainly are seeing it. We're seeing worker co-ops that are finding ways to adapt their business model, knowing that even if things re-open right now, that they see an opportunity to create more virtual or online opportunities to sell their products or services. And we see we see that.

So we've had folks coming to us or loans to add on new parts of their business, even in the midst of this. Not because they aren't experiencing crisis, but they found ways to kind of grow from this in a new way. So I guess as nervous as I am about what's coming down the path, and as concerned I am for the health and safety of our members, I do see an opportunity for worker co-ops. I think they are a key part of the solution going forward, because they're looking out for their workers in ways that other businesses just often fail to do. And I think they are able to be to kind of find ways to adapt more creatively too, because they get the buy in of the key people, the employees. So I think there's opportunity for startups and a lot of opportunity for converting businesses where the owner may just say, "I can't do this alone. I can't navigate this alone." But their employees may say, "You know what? together we can do this. There's a business here that still is needed, that we still want to work in. So if we work together, we can be successful. So I am optimistic that through all of this, this could be, in fact, a key opportunity to grow more worker co-ops, and really have more of the mainstream economy recognize the value of cooperatives broadly, and worker cooperatives in particular.

MJ: I think one of the things that I have learned over the years that supports your outlook: if you're optimistic -- not unrealistic, but optimistic -- you're going to see the opportunities, more likely than if you're pessimistic. The Grays in the darkness cover up what's out there.

Christina, thank you very much. This has been very informative, for me at least. And I certainly hope that it's been informative for all the people who are going to view our videocast.

And best of luck. And maybe we'll run into each other at some conference along the way over the next few years.

CJ: Thanks, Michael really nice to talk to you. Thanks so much for inviting me on.

MJ: So this has been an interview with Christina Jennings of Shared Capital Cooperative. And this was done by the Grassroots Economic Organizing newsletter. I'm Michael Johnson. And thank you for tapping into it. Have a good day.

This transcription has been lightly edited for readability.

Citations

GEO Collective (2020). Shared Capital and Solidarity: An Interview with Christina Jennings. Grassroots Economic Organizing (GEO). https://geo.coop/articles/shared-capital-and-solidarity

Add new comment