Introduction & Preface | Chapter 1 | Chapter 2 | Chapter 3 | Chapter 4 | Chapter 5 | Chapter 6 | Chapter 7 | Chapter 8 | Chapter 9 | Chapter 10 | Chapter 11 | Chapter 12 | Chapter 13 |

Translator’s note:

What form should member ownership take in a worker cooperative? How is the form of ownership related to the economic viability of the enterprise? How is ownership of equity allocated and measured, what impact does ownership and accumulation of equity have on distribution of surplus?

In Chapter 4, Luis Razeto analyzed the distinctive features of accumulation in workers enterprises. In this chapter, he offers an economic theory of ownership and distribution of surplus in worker enterprises, proposing the issuance of “labor shares” representing individual members’ ownership of equity. He also proposes including both member contributions of direct labor and their contributions of factors embodying “objectified” labor in the calculation of surplus allocations.

As Razeto advances in his analysis of cooperative economics, he continues to introduce new terminology and re-define existing terms. For example, when describing the equity of a workers enterprise, he places “capital” in quotation marks, indicating that the economic assets in question, which are situated within non-capitalist relations of production, are not operating as capital in the strict sense. While he uses the mainstream economic language of factor productivity, it is for the purpose of formulating a theory of surplus distribution that combines efficiency and fairness.

Readers familiar with marxian political economy may be confused by the use here of familiar concepts. Razeto employs a concept of simple labor time that is similar to that used by Marx, who refers to “simple labour-power.” While for Marx, who was analyzing capitalist production, it was crucial to distinguish between constant capital, variable capital, and surplus value, for Razeto the key distinction is between external factors, obtained on the market, and internal factors contributed or created by workers. It is on the basis of member contributions of internal factors – both direct labor and previous, “objectified” labor – that surplus is distributed and reinvested or accumulated.

While it may be hard going at points, the promise of this approach is a framework for economic analysis that highlights and clarifies the relations and operations of worker cooperatives, instead of obscuring and confusing them through the misapplication of concepts developed for the analysis of a very different system.

- Matt Noyes

Chapter 5

Ownership of cooperative equity and distribution of surplus and profit.

1. Understanding the formation and expanded reproduction of equity (whether in the form of Labor or Community) in cooperative enterprises in the way that we have presented implies a profound reconsideration of the theme of cooperative ownership. It also implies the necessity of specifying the criteria for patronage allocation of surplus in this type of enterprise, which leads immediately to a third issue: how to treat labor.

The theoretical treatment of “capital” and surplus in cooperatives has been obscure, resulting in an abstract and generic formulation of the concept of ownership as a prior assumption, instead of a formulation based on the real relations and economic rationality of these enterprises. People habitually refer to the social character of cooperative ownership without paying much attention to its concrete mode of formation and expansion and without realizing that by simultaneously affirming the private character of the benefits distributed to members they fall into a deep contradiction. Once again, the result is great error and confusion, which manifests in an excess of ideology and a paucity of theory.

The concept of social ownership of the means of production has been used to shield cooperativism from the accusation that it fails to radically overcome capitalist social relations of production. But in fact, the concept of social ownership is merely standing in for the lack of a theory of the content and composition of cooperative equity; almost as if by simply defining cooperative ownership as “social” one were preventing it from being capital, or at the least exorcising all negative connotations. Social ownership of the means of production, it is assumed, would imply a guarantee of democratic, communal, and participatory management. All of this is evidence of a lack of transparency in the traditional doctrine and practices of cooperativism, since the ideological affirmation in some way papers over the real social relations at work in cooperative production.

There has been no lack of doctrinaire discussion of forms of cooperative ownership, and this has given rise to various practical approaches. The following are the most wide-spread forms of ownership in the cooperative and self-managed sector:

a) Collective ownership: ownership of equity is held by the members or participants in an economic unit, as a group, with no assignment of shares to each person, and thus no way to recover one’s individual contributions upon retirement.

b) Collective ownership with recognition of individual money contributions: the group is the owner, with no differentiation between the part of the equity comprised of donations made by individuals and that which comes from reinvestment of surplus generated by the enterprise itself. In return, individual contributions of dues or savings invested in the cooperative are recognized as property of those individuals, recoverable upon retirement from the association.

c) Individual ownership, collectively managed: the equity of the cooperative is in this case the sum of individual contributions which remain tied to the individual members who make them. Gains generated by the operation of the enterprise are allocated to members, with the exception of a percentage that is held to cover general administrative costs. This is the case in housing cooperatives, credit unions, producer cooperatives and other organizations which have the character of associated management of individual economic activities for purposes of economies of scale and other opportunities.

d) External ownership: financial and material means of production are provided to the enterprise by an external economic subject that remains their owner. The enterprise leases these assets without a time limit, paying the owner (the State, a foundation, or other) a fixed rate or levy. Gains generated are allocated in their entirety to the worker-members, who use and manage the external capital in a relatively autonomous manner. This form of ownership has spread among “self-managed companies” in which there is a distinction made between ownership of capital and its use and management.

These different forms of ownership give rise to enterprises operating with different economic logics. We refer to these throughout this book – most often critically – when addressing particular problems that affect enterprises organized by the Labor category that operate in the “market economy.” In fact, there is no inherently rational and adequate form of ownership. Whether a form is rational depends on the organizing category, the type of market or economic relations in which the enterprise operates, and various other aspects that have an impact on their operational logic and rationality. Thus, various forms of ownership can coexist within the cooperative phenomenon, corresponding to the different rationalities at work, which, in turn, are based on the organizing categories of Labor and Community.

2. Moreover, the concept of ownership itself needs to be explored before we can judge which form is best suited to a given case. Here, too, it is necessary to undertake a process of conceptual re-elaboration so as to arrive at an autonomous standpoint on which a better theory and practice can be based. Before we continue with our analysis, then, we must prepare the conceptual tools needed. In this case, the concept of ownership.

As we did with the concept of the enterprise, we can start from a concept of ownership that is broad enough in formal terms to include various forms and possibilities, even if it does not contain or sufficiently explain them or their contents. With such a concept as a point of departure we can later specify the implicit contents and different alternatives.

In generic terms, ownership can be defined as the right an individual or collective subject obtains to consider an economic good as its own and to dispose of it at will, within the established legal frameworks that recognize and guarantee the right of ownership. This concept includes the essential constitutive elements of ownership, which it is nonetheless necessary to define more specifically if we are to reach an adequate comprehension of the reality it seeks to apprehend.

The aspect that stands out most sharply is that ownership is a relation between a subject and an economic object. We can distinguish three inseparable elements of ownership: the subject, the object, and their nexus or relationship. The three elements can shape the ownership relation in different ways because the subjects, objects, and nexuses involved can themselves vary. Nonetheless, they do not have equally strong impacts when it comes to determining the mode of ownership. In the ownership relation, the subject predominates over the economic good insofar as it is the holder of the right, and thus the active element, while the economic good presents itself as the passive element, the object to which the right acquired by or held by the subject applies and upon which it is exercised.

The subject may be individual or collective. This does not mean that there are only two subjects who are entitled to own property (the individual and the State) but that there are two modes of constitution of a wide variety of economic subjects. Not only individuals and the State, but local communities, enterprises, private and public institutions, families, associations, etc. can all be subjects with ownership rights. Keeping in mind this element of the ownership relation – the subject to whom the right of ownership is attributed – we can distinguish among various types of property: personal private property, shared personal property, family property, corporate or share-holder property, associated or group property, cooperative property, community property, local collective property, national collective property, government property, institutional property, international property, distributed property, forms of property combining two or more of the above, and still more.

Taking into account both the subject (the owner) and the various forms it can take, we come to understand that the forms of ownership correspond to the degree of constitution of the subject. Thus, in order for communal property to exist it is necessary that a real community, constituted as a subject, exist. If not, we are dealing with a fiction. In order for national property to exist there must exist a nation constituted as such and in some way self-aware; likewise in order for state property to truly be a form of national property, the state must effectively represent the national community and not just the class or constituent group that occupies a dominant position. There can no collective ownership by workers in an enterprise in which the group of workers has not yet formed the collective consciousness and will required in order for them to function and be recognized as a collective subject. And so forth in many cases.

Turning to the objective element in the property relation, generally speaking ownership pertains to economic goods. Thus, the various factors of production that have economic value can be property and the objects of ownership. In other words, in enterprises, ownership applies to and is exercised over not only the material means of production (land, buildings, equipment, implements, machines, raw materials, processed products, etc.) but also labor power (the physical and intellectual capacities that are activated in economic processes, including professional qualifications), technology (information, design, technological systems, etc.) management or administration (management conditions, administrative skills, decision-making power, etc.), financing (money and other means of payment, potential credit, etc.) and even community (belonging to the group, capacities of integration, values, social relations, etc.).

These different types of economic goods (in this case, factors of production) are the objects of appropriation by economic subjects, and, most important, remain particular established modalities of property rights. (This is so even when not all of these modalities are recognized juridically. In fact, one sees an evolution of rights: whereas in Roman Law property was understood to apply exclusively to “corporeal things,” today we recognize property rights over intangible goods: intellectual, technological, relational, administrative, etc..)1

This aspect of the concept of ownership is particularly important to grasp given all that we have said about equity and how its content varies in the different types of enterprise, according to their different organizing categories. In effect, a factor is owned by the subject who personifies it, that is, who brings it to the enterprise. When defining the form of ownership of a given enterprise, one refers not to the specific combination of factors which it comprises, but only to those factors which “belong to it” and form part of its equity.

Finally, regarding the nexus between the different economic subjects and goods, additional important distinctions must be made. In effect, rather than a simple nexus we are dealing with a structured complex of relations.

The first thing that stands out in this definition of ownership is the juridical connection, a right, indicating that, whatever the origin or source of the ownership, its legitimation or social recognition is essential, in accordance with the terms that society has established, and always subject to some legal limitations.

But the juridical connection is only the first aspect of the ownership relation. There are two others. The second is the consideration of the economic good as one’s own, that is, a feeling of ownership that distinguishes one’s own economic good from something owned by someone else. This subjective and psychological bond between the subject (a person or collective) and the object or good (economic factor), has cognitive, affective, and volitional connotations. Through this bond, the subject knows that the good belongs to them and feels that it is theirs, which implies (and suggests to others) that the subject is prepared to defend their property with some degree of conviction and demand that their right be respected. It is because of this subjective bond that we can understand property as something that can be “violated”, “respected,” “exploited,” etc., terms that refer not only to the economic factor but to the affected subject.

The third aspect of the ownership relation is the subject’s right to dispose of the good as they like. This makes it clear that ownership is a power relation, in which the subject controls and can dispose of, use, direct and consume the economic good as they see fit. This implies, on the part of the subject, the exercise of freedom and the capacity to make decisions, which supposes, at the same time, the understanding and control of the activity and the mode of operation of the factor in question.

There is, too, a restriction with respect to the power and liberty of subject to dispose of the object: legislation establishes the framework within which the decisions made by the subject with respect to their property are recognizable as legitimate. This reveals a final decisive aspect of ownership relations, that is, that society as a whole reserves for itself some right over goods that are privately owned: there is no such thing as absolute and unconditional ownership. There is a kind of “social mortgage” on all property, as His Holiness John Paul II put it in Sollicitudo Rei Socialis, which requires that all property be utilized in view of the natural qualities of the object and the common good, taking into account the rights of others and the social dimension inherent to all human activity and relations.2

If we now consider the different aspects and elements of the complex relation of ownership and property in their unity, we can understand that ownership is less a fact or data point, than a process. We underscored this in the initial definition by using the verb “acquire” instead of “have.” Naturally, ownership endures over time, but it varies and changes in accordance with modifications that take place as much in the subject as in the object and in the ties that bind them. In practice, the bonds of ownership are formed and dissolved, strengthened or weakened, depending on the degree of coherence or dissolution of the subject and the degree to which the different aspects of the relation between the subject and the good or factor in question are strengthened, weakened, or altered.

One does not acquire ownership of a good produced in a complex process through the simple juridical act of acquiring a title to it. On the contrary, ownership arises through a complex process of progressive appropriation, which implies a subjective process through which the owner (individual or collective) assumes consciousness of ownership, acquires the feeling that said good belongs to them, and then comes to know, dominate, take possession of, and make decisions relative to the economic good which they have incorporated into their equity.

Clearly, when the subject of the property right is an individual, the right of appropriation is fulfilled fairly quickly and sometimes even instantly; but when the subject is a collective or a complex organization, the acquisition of ownership can require a lot of time and effort. In some cases it is conditioned by a collective process of maturation and subjective development through which the collective, group, or community constitutes itself as a self-aware subject endowed with will and autonomy. Such complexities are observed, for example, in the case of the conversion of a capitalist or State firm to a workers collective or cooperative.

On the other hand, it often happens that the process of appropriation begins not with the establishment of the juridical connection but through a progressive assumption of ownership which begins with understanding the good or factor of production and developing the capacity to use and control it, leading to the feeling of ownership. Only in a later step does all of this come to acquire the juridical form of a socially sanctioned right.3

This also enables us to understand that the process of appropriation of each of the different factors can follow a particular path. The process of appropriation of a material factor of production is not the same as that of a technological or administrative factor. Appropriating a technological factor may require a specialized process of study, and its juridical sanction may require acquisition of a professional title or academic degree, or securing the right to use a brand.

3. Having understood ownership as a complex process, we can see the problems posed by cooperative or self-managed property in a new light. We can now describe, moreover, some facets of social and political processes that are habitually ignored. But, let us stick to the specific question of the forms of ownership and equity in enterprises organized by Labor and Community.

Up to now we have referred to forms of ownership of economic goods and factors in general; but we know that the combination and organization of factors in an enterprise poses a decisive question, that of ownership of enterprises and within enterprises. In keeping with the concepts deployed so far, clarifying this requires us to pay attention to the subject and object of ownership as well as the mode in which the relationship between the two is established.

Who is the owner of an enterprise? How is equity appropriated? How does ownership expand as the business generates surplus? How intense is the relationship between ownership and equity, and in what form is it established? All of this depends above all on the organizing category of the enterprise, the economic category which subordinates, subsumes, and puts into operation the factors gathered under its control and management. Thus, for example, the subject, the object and the mode of ownership corresponding to an enterprise organized by the category Capital are different from those corresponding to another in which the organizing category is Labor, and, in the same way, the types of ownership corresponding to enterprises organized by the other categories are also different.

This is easily understood if we consider the different subjects that correspond to the respective factors which comprise organizing categories: landlords who possess material means of production (land and buildings), capitalists who possess money for financing, workers who possess labor power, communities that possess the “C Factor,” managers and administrators who own the administrative factor, engineers and technicians who represent the technology factor. All of these subjects have different qualities and characteristics. The organizing category organizes, subordinates, subsumes, and lends its own form to the factors it incorporates into its equity. It relates to them in accordance with its way of being and acting, appropriating equity in its own way and imposing on the enterprise an ownership “regime” that is characteristic and unique.

But the form of ownership depends not only on the subject, even if the subject is the more important element in the relationship; but also on the object, that is, on the equity, which as we have already observed presents different objective and subjective contents in each type of enterprise. It should be noted that ownership is naturally exercised by the subjects who contribute factors to the enterprise. The distinction between internal and external factors derives from precisely this: some factors have been incorporated into the equity of the enterprise, contributed by the organizing subjects, and some have not.

Now, whether internal or external, factors have different degrees of personalization, or put differently, are more or less separable from the subjects who contribute them to the enterprise. For example, labor power is inseparable from the subjects who contribute it, because it is a matter of the physical and moral powers of human beings as such. Techniques have a high degree of connection to the subjects who have developed them, but they can be separated from their creators and transferred to others through a process of training or apprenticeship. They can also be objectified in physical objects, in designs and models separable from the subject and as such transferable. The same is true, in different ways, of each of the other factors.

So, ownership of equity is directly shaped by the factors comprising that equity, which differ according to the type of enterprise. For example, insofar as labor power is inseparable from the workers who contribute it, it will necessarily constitute an external factor in an enterprise in which the organizing factor is something other than Labor or Community; this is a structural condition of such enterprises. In a workers enterprise, on the contrary, the finance factor may initially be external only to be incorporated into the equity of the enterprise through credit of one form or another.

Based on this we can see that it is possible, and may be necessary, to distinguish between one or another type of ownership of equity in a given enterprise, depending on the factors comprising the equity.

We can now make a double distinction: in addition to the distinction we made before between internal and external factors, we can now distinguish between factors that are more or less inseparable from the people who contribute them: “human” factors, inseparable from their contributors, and “objectified” or separable factors. Applying the two distinctions we can differentiate between four dispositions of factors: internal human factors, external human factors, internal objectified factors, and external objectified factors.

With these theoretical specifications in hand we can now analyze and resolve the question of ownership in cooperative enterprises. For now, we will only consider worker enterprises, those in which Labor is the organizing category. (Community or communal enterprises require a different treatment which we will not provide here, although the criteria and analyses we have provided offer sufficient antecedents to resolve their particular economic rationality.) Let us begin where we left off in the previous chapter.

We demonstrated that equity in worker enterprises does not have anything to hide, nothing to be ashamed of, because it is essentially Labor: accumulated internal labor, current internal labor, and anticipated internal labor. The nature and composition of the equity, subsumed under the form of a given category, in this case Labor, defines the character of ownership. Thus, one must logically conclude that ownership based on Labor should not be considered generic social ownership but personal ownership by the workers who are associated in the enterprise and are its owners.

To call this form of ownership personal is to affirm its private – and not “social” – character; though it should be noted that the term “social” is ambiguous: first of all because private ownership is typically opposed to “public,” not social, ownership, and secondly because “social” can comprise more than one form of relations, not just public, but also communal, associative, collective, etc. In fact, when referring to the property of worker enterprises we intentionally defined it as the personal property of associated workers, and in so doing recuperated a social aspect – association.

It is necessary to deepen this concept, unraveling all its implications and examining its effects at the level of the structure and functioning of this type of enterprise.

By affirming the personal character of ownership we distance it from the habitual notion of social ownership, underlining the fact that in this type of enterprise equity is assignable to concrete people who work there in association and not to the “collective” of workers as such (in which case the precise amount of equity belonging to each worker would be irrelevant).

This affirmation may seem to contradict the characterization of labor as social and collective: if productive labor is inherently social, how can we define ownership of labor, as equity, as something private and personal?

The contradiction is only apparent: the social nature of labor refers to the fact that organized production can only take place through the combination and technical and functional division of a group of workers, each of them an element in a complex labor process. In other words, the labor power of individuals converts itself concretely into a productive force to the degree that it is socially organized.

Thus “social” labor should not be understood as “joint” labor but as labor in cooperation. Association does not presume the dissolution of individual workers in a generic collective subject but rather presupposes and recognizes the personal character of the contributions made by each worker in all their particularity. The cooperative association of workers is the superior and most coherent expression of the essence of labor, and from it we derive the formulation of ownership of equity as “the personal property of associated workers,” which can also be termed associated personal property.

Ownership is a right to equity, in concrete terms the right freely to use and dispose of equity (within certain juridical limits) and the profits and gains resulting from its commercial or productive use. So who has the right to dispose of labor power – all the more when that labor power has not been rented to others – but the workers themselves, who possess it? And who has the right to the results of its application, that is, the value created by the labor performed? Who but the person who did the work can legitimately appropriate this?

It is true that individual labor power is productive insofar as it participates in a process of labor in cooperation and that labor itself is organized in an associated way. This is why the wealth created in the process can be considered gains of the enterprise, one part of which can be legitimately reserved in order to add to the equity in the form of the additional productive and economic factors needed to reproduce and grow.

This associative and cooperative character of labor is the basis of the right of the cooperative enterprise to establish statutory and regulatory frameworks with regards to the personal appropriation of equity. It is also the basis of the right to decide how much of the gains will be destined to increasing the equity and how much will be distributed directly to the workers.

Nonetheless, when it comes to this equity and this surplus, however it is used, each worker maintains an inviolable personal right in proportion to their specific contribution. In concrete terms: if one member has contributed 200 days of labor to the formation of the equity and another only 120 (assuming a homogeneous day of labor), it is obvious that the equity of the enterprise will have gained more from the first member than the second, and thus that the share of each in the cooperative property is different. If this difference were not recognized at the level of ownership it would amount to a transfer of value from the person who worked more to the person who worked less, benefiting the latter and penalizing the former.

If the workers’ right to personal ownership of equity and surplus were not recognized, and more specifically, if the portion of the surplus they create that is reinvested were incorporated into the equity without differentiation, dissolved into common property of the cooperative, and if the worker were to lose this property upon leaving or retiring from the enterprise, it would amount to true exploitation of the worker by the cooperative. In such a situation, it would be natural for each worker member to resist “capitalization” or growth of the enterprise through reinvestment of part of the surplus for productive ends.

Thus we see how justice and economic logic coincide with operational efficiency. In cooperative production, the logic of expanded operations requires us to consider cooperative property as a form of personal property which is not “social” in the sense of jointly held. While it is personal property, it is not capitalist, and there is nothing shameful about it. This equity is not built through a process of accumulation of extraordinary profits derived from paying wages lower than the productivity of labor. Moreover, the equity produced by many is not the property of a few but shared among all the people who participated in its creation, in proportion to their contributions.

We spoke earlier of “personal associative property.” It is equally appropriate to describe this type of ownership as “distributed personal property,” a formulation which highlights the difference between this and other forms of private property which imply a growing concentration of equity. While it does not necessarily entail the division of ownership into equal shares, distributed personal property describes a process of proportional and equitable distribution which can not lead to large discrepancies in ownership stake.

By affirming the personal, not shared, character of ownership in the workers cooperative we are establishing a theoretical criterion that corresponds to a logic of rational operations. This notion of cooperative property, however, is often not recognized in the laws which govern cooperative enterprises, and, in some doctrinaire formulations of cooperative theory, is even doubted or rejected. Our notion undoubtedly has practical implications, in so far as the recognition of the personal character of cooperative property translates into a different enterprise structure than that which prevails in many traditional cooperatives and self-managed enterprises. The structure differs, in particular, with respect to the decisive question of the treatment of economic factors. This question, which conventional economic theory formulates in terms of the relationship between capital and labor, must also be addressed in our special theoretical framework. We have already seen that the cooperative experience has presented problems that limit its efficiency precisely around this question of the treatment of economic factors.

4. It is opportune, then, for us to pause to consider how worker enterprises can structure themselves in order to operate rationally in the market, in accordance with the distributed-personal-associative character of cooperative equity. The elaboration that follows amounts to proposing a new mode of organization and operations, one that can be adopted by workers enterprises, worker cooperatives and other enterprises founded by Labor.

To be more precise, we need to distinguish between internal and external factors, as well as between those that are human and objectified.

With respect to external objectified factors, which typically take the form of financing obtained through credit, and material means of production bought or leased on the market, we have already clearly established the necessity and appropriateness of treating them the way they are treated in normal market relations.

With respect to external human factors (with the exception of labor power which we will consider in the next chapter), that is, with respect to the technological and and administrative factors associated with people – that is, with the technicians and administrators who contribute them – it also makes sense, in general, to treat them in accordance with normal market terms. In concrete terms, this means hiring engineers and technicians, as well as managers and administrators, as needed for the functioning and operation of the enterprise, that is, when the workers who organize the enterprise lack the required technical and management capacities. Nonetheless, and precisely because we are dealing with human factors in the sense that we specified before – people who have some influence in decision-making and governance of the enterprise – the special importance of their incorporation in the enterprise in order to assure its self-managed character is worth mention.

These factors can be appropriated in two main ways: through recruiting technicians and administrators to be members of the enterprise, valuing their labor as highly qualified, or through a progressive appropriation of the skills that they apply in the enterprise, for example through a collaborative process of training and apprenticeship, in which skills are transferred from the specialists themselves to the workers who are most ready to acquire them.

An enterprise that adopts this perspective for the medium or long term, should, when searching for contributions of such factors, take into account other dimensions not included in standard market categories of price, quality, contact terms, etc.

When it comes to the internal factors, we must address the question of the enterprise’s ownership regime, given that we are dealing with its equity. The internal human factors pose two problems, one theoretically simple and the other rather complex. It is very simple to determine who owns internal human factors since they are inseparable from the concrete people who represent them and contribute them to the enterprise. Individual members contribute labor power (the physical and spiritual capacities of the worker as a person) in varying degrees; they contribute administrative and leadership capacities, and knowledge or technological skills, including their values and relations that are unifying, convivial, and solidaristic (“C factor”). Of course members can communicate, share, and spread these values among their co-workers but in doing so they do nothing more than share with others that which before only they possessed. Different people contribute the various productive factors through showing up and being active in the enterprise, raising no questions about to whom the factors correspond or belong.

However, a complex problem arises with regard to the measurement of internal human factors, since not everyone contributes factors in the same quantity or with the same qualities.

But, one might ask, why do we need to measure them?

The answer is, because internal human factors are not all equally productive. The contribution made to the product by an unskilled worker is not the same as that made by a specialist technician; the contribution made by an expert in administration is not the same as that of a worker who lacks knowledge of markets and management; the contribution made by the person who originally conceives of the product or designs it is not the same as that of the person who reproduces it. Evaluating and measuring all of this will be decisive when it comes to distribution of surplus among the members in proportion to their effective contributions to its generation.4

In the case of objectified internal factors, the problem of quantifying remuneration is easier to resolve precisely because of the objective nature of the contributed factors. Still, a crucial and decisive question of how to assign ownership of these factors is posed. We are dealing with factors that are present in the enterprise because they have been contributed by members or generated through the operations of the enterprise itself. They belong to the members because of the particular form of ownership that corresponds to a worker enterprise. But, this does not resolve the question of the proportional distribution of ownership of objectified internal factors among individual members.

Analytically, we can distinguish between these problems – quantifying remuneration and assigning ownership – focusing first on the problem of measurement. Whether we are dealing with human or objectified factors, it is first of all necessary to identify the unit of measurement to be used: a homogeneous standard of measure that will serve in both cases.

In corporations the units of ownership are shares of stock, each of which represents abstractly one portion of the total equity of the enterprise and has a specific nominal value (corresponding to its money value at the time of issuance), a book value (corresponding to the value of the enterprise’s assets divided by the number of shares issued), and a market value (corresponding to the valuation of the stock in the capital market or stock exchange).

The ultimate unit of measurement of capital (in capitalism) is money, which represents the simple and elemental form of the finance factor on which the capitalist enterprise is based. Capitalist enterprises measure equity using specific amounts of these units of money, in the form of stocks.

The first thing we need to establish is that in workers enterprises the units of ownership are not units of capital but units of labor, which represent, abstractly, a specific quantity of equity. Here, too, the unit of measurement corresponds to the simple and elemental form of the factor on the basis of which the dominant category is these enterprises is determined, in this case, labor power.

The natural measurement of labor power, its simple and elemental form, is given in units of simple labor. This means that the total equity of the enterprise and the participation of each worker in its ownership has a precise equivalent in units of simple labor, and can thus be quantified. Because labor time is expressed in hours of labor, or alternatively, work days, the equity of worker enterprises is expressed in hours or days of simple labor. (The expression “simple labor” will be clarified later on. For now, one can understand simple labor as the labor performed by unskilled labor power, that is, the application as part of the enterprise’s labor power of the productive capacities that any normal person without any particular acquired expertise or specialized training might possess.)5

This unit of measurement of labor finds a monetary equivalent in the market, and in that sense, at any given moment, it can be expressed in units of money.

We can say the same thing another way: at any given moment, units of measurement of capital, that is, money, find in the market an equivalent in the form of labor power, and can thus be expressed in units of labor time. If for example, one hour of simple labor is worth one dollar, it is also true that one dollar is worth an hour of simple labor.

This means that the units in which the distinct factors are expressed in the market are reciprocally convertible. This convertibility facilitates contribution accounting because it means we can make use of the system of prices by which the market provides fairly reliable indications we can use when quantifying the effective contributions of factors and the distinct elements of equity.

Armed, then, with a unit of measurement of equity (simple labor), it is possible to assign to each member in a worker enterprise that part of the ownership of equity that corresponds to their personal contribution. We can imagine and implement a system of “shares” in which each share is equivalent to the value of a work day (or eight hours) of simple labor carried out in the enterprise. For functional and accounting purposes it does not matter if we call these units shares, bonds, parts or some other term. What matters is that they represent quantifiable units of equity expressing values that are variable, as we will see, equivalent to a determinate amount of labor.

For purposes of exposition we will call them labor shares or cooperative shares. Let us see how this works.

5. In the first place, we need to specify that while all the equity can be measured in units of labor time, this does not mean that all the equity should be converted into labor shares.

In effect, labor shares are necessary and useful only for those factors that we identify as internal objectified factors. As we have seen, there is no problem assigning ownership of internal human factors, which belong to the person who contributes them. The quantification and valuation of equity is also important for the purpose of identifying the portion of surplus (objectified) that is to be distributed on the basis of a member’s contribution to the product. We will proceed one step at a time, taking care to distinguish between the different situations and problems.

The portion of equity which should be expressed in labor shares is the part made up of internal objectified factors which include various factors with different sources. We can distinguish between:

a) the objectified factors initially contributed by members, necessary for the establishment and putting into motion of the activities of the enterprise; and

b) that part of the surplus generated by the enterprise in its continuing operations that is not distributed to members but re-invested in the enterprise or placed in a reserve fund.

Both components of cooperative equity should have a corresponding value in the labor shares to be issued by the enterprise. But, the measurement of the value of each component requires different procedures.

The member’s initial contribution of objectified factors may be made in various forms: basically, money (finance factor); facilities, equipment, or machinery (material factor); product models and designs, processes, technical systems, copyrights and patents (technology factor); administrative capacity and transferable client lists (administrative factor).

All of these contributions can be evaluated, valued, and measured. In each case, they consist of certain quantities of units of labor. In some cases, it is labor carried out in the current enterprise. In others, it is labor previously done which has been accumulated or saved (usually the product of labor the member has done in some other activity or economic unit). This accumulated labor comes to represent a quantity of units of labor once it is incorporated into the workers enterprise and thus converted into Labor (the dominant category).

The issuance of labor shares is based on measurements of hours or days of simple labor. But, to which days of labor do we refer? The evaluation and measurement of days of labor must be made by the members themselves, in the course of forming their association.6 It will probably be a process of negotiation, but not arbitrary. In effect the members have two sources of essential and indispensable information.

On one side, each of these factors finds equivalents in the market and has an alternative cost: the price the enterprise would have to pay to obtain them from external sources. In lieu of contributing them to the enterprise, the members could place on the market the factors they possess and receive a specific remuneration. The sacrifice of this remuneration is what economists call “opportunity cost.” Thus, one can determine the money value of all of these contributions by using “opportunity costs,” the values being summed and attributed to the people who contributed them, in a process that determines the total value of member contributions to the enterprise as well as the amount corresponding to each member.

The problem, then, is to determine the amount of money that corresponds to a unit of simple labor. At the outset, when the enterprise initiates its activities, the value of a day of simple labor is not yet known; but it is not important. The initial factor contributions correspond to previous labor (accumulated in the ways specific to each factor), so their equivalent value in units of labor can be established by converting the average or normal remuneration received by simple labor on the market into hours or days of simple labor.7 If one wished to be more exact, one could consider the remuneration that one would pay for the equivalent quantity of simple labor in similar enterprises, of the same scale, type and technological composition.

To know how many shares to issue and assign to each member it is enough to divide the amount of the contributions made by each member, measured in monetary values, by the value of the simple day of labor. Let’s look at an example.

Let us suppose a small enterprise formed by three workers: Pedro, Julia, and Diego.8 Each makes an initial membership contribution of $10,000 in cash. In addition, Pedro contributes material means of production valued at $30,000, Julia contributes $15,000 worth, and Diego does not contribute any material means of production but instead contributes technological and administrative factors (models, production designs, a client list, and business experience) that have been valued at $40,000. Such are, in this enterprise, the internal objectified factors, with a total value of $115,000. Let us suppose now that a day of simple labor has been valued at $100, based on the standards of the market. The enterprise should issue, then, shares totaling $115,000, that is, 1,150 shares of a nominal value of one day of simple labor. Those will be assigned to Pedro, Julia, and Diego in the amounts of 400, 250 and 500 shares, respectively.

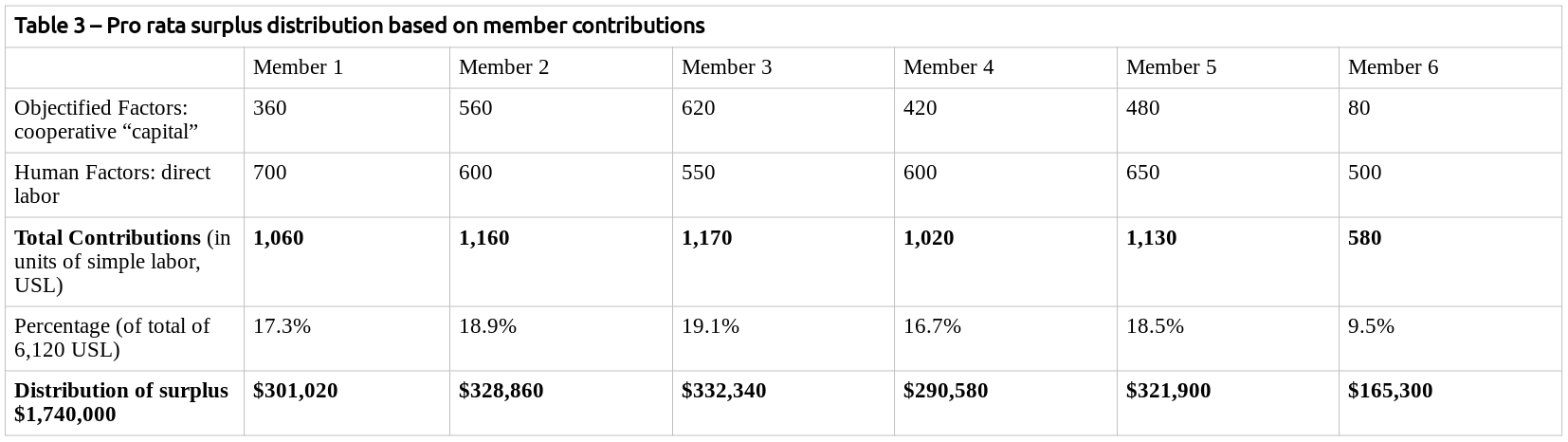

Let’s look at are more complex case. Consider six members who contribute different quantities of the four objectified factors, assuming a day of simple labor equivalent to $500.9

Now, given this composition of the portion of the initial equity consisting of objectified internal factors, let us assume the equity increases at the end of the fiscal year as a portion of the surplus is reinvested or added to the reserves, instead of distributed to members.

In capitalist corporations this accumulated value is recorded as an increase in equity and reserves with no corresponding increase in the number of shares, though the existing shares may increase in book and commercial value. (The accumulated value does not correspond to an amount of cash, but rather a specific net increment of the equity of the enterprise; “net” insofar as depreciation has been subtracted.) In worker enterprises, on the other hand, growth in equity should result in an annual issuance of new shares, allocated according to the number of working hours or days which went into generating the newly reinvested portion of the surplus.

It is not enough to simply revalue the existing shares in monetary terms because, as we know, the relevant unit of measurement is labor time and not money. (One might think of revaluing the shares in terms of hours or days of labor, for example, establishing a book value for the shares equivalent to more than one day of labor per share (or less, in the case of losses), for example 1.16 days per share, or 13 hours of labor per share. In terms of valuation of the global equity, this would have the same effect as issuing new shares, however, it would create a new problem when it comes to allocation, to which we will refer shortly.) It is also worth noting that issuing shares does not necessarily mean printing certificates and signing them over individual members, it being sufficient to keep duly protected records for each member.

To determine the correct number of labor shares to be issued in accordance with the increase in equity it is not necessary to have recourse to an external criterion like the one we indicated for the initial capital contributions, since we now know the amount of labor that generated the value and can derive an exact figure.

We know that the total net gains in the fiscal year (that is, the sum of the anticipated distributions made to compensate workers for direct or actual labor plus the amount of surplus that has been reinvested, plus the amount that remains available after taxes and depreciation) have been generated by, and in that sense are equivalent and correspond to the total number of days of labor utilized in their production or generation. (To refute this affirmation one might argue that the surplus has been generated by the all of the factors used, including external factors, be they financial credit, leased machinery, wage labor, etc. But this is not the case. While all of these factors have contributed to the gross revenue, when calculating the surplus the payments made for external factors are deducted, in accordance with their respective contributions.10) That which has contributed to the generation of surplus is labor, that is, accumulated or previous labor plus the current or direct labor concretely deployed by workers during the period or fiscal year in question, in the form of direct labor. In other words, labor in the form of objectified internal equity as well as direct labor and the other internal human factors. (It is precisely the necessity of accounting for the various contributions of this factor (Labor) that led us to reject the alternative of revaluing the existing shares instead of issuing new shares. There is no guarantee that the contributions of direct labor will be proportional to those made in previous labor.)

Let us suppose that the enterprise in our example in the previous table generates a net surplus of $1,740,000 and that the workers performed in all 3,600 days of simple labor. (We will explain later how we arrived at that latter number, for now let us assume it.) In this case, we can see that the surplus is the product of a total of 6,120 work days: 3,600 work days in this cycle, plus 2,520 days of simple labor performed in previous cycles and embodied in labor shares. As a result, the current value of a unit of simple labor is $285.11 (Not a great year for the enterprise, but not too disappointing for a first year in operation.)

Now let us suppose that the $1,740,000 surplus is divided among the members in the following ways: $1,440,000 in anticipated distributions, averaging $20,000 monthly per member, and $300,000 reinvested in the enterprise, added to the equity.12 The new shares issued by the enterprise are shares of the amount added to equity. As the current value of the simple work day is $285, a total of 1,052 new labor shares will be issued.

One can see that the value of the labor shares has fallen. The previous shares were valued at $500 and the new shares are $285.13 This is of no importance from the point of view of the ownership structure, since the equity is measured in shares whose nominal value is always equal to one day of labor. It is the change in the value of a day of labor in the enterprise that is causing the shares of equity to lose value, which is, moreover, relative: each member will have more shares of lesser value and the total of each member’s holdings will be slightly higher than the previous year, due to the small increase in equity. Nor will the changing share value change member’s relative participation in the ownership of the enterprise.

The falling value of the labor shares will nonetheless serve as an indicator that the enterprise is operating inefficiently, insofar as the same factors could be more profitably placed on the market. It is, in any case, a manifestation of the risk taken by the founders and organizers of the enterprise. (If the members understand that their share of the equity might make more money if it were invested outside of the enterprise they might opt to liquidate the enterprise and place the funds and assets on the market; such a move has its costs which should also be evaluated. Above all, it would be wise to do a serious evaluation of the future projected earnings of the enterprise, which might offer better prospects than liquidation.)

If the surplus generated in the current period is inferior to the amount distributed to workers in the form of anticipated distributions, we would find ourselves in a situation in which the enterprise produces not gains but losses, with the result that the equity of objectified factors, instead of increasing, would have fallen.

The task is to determine how many days of labor correspond to the losses of the enterprise, so as to be able to carry out a reduction of shares (or an issuance of negative shares, on the same pro rata basis: in proportion to the portion of the total shares held by each member). The procedure for calculating how many shares would be deducted (or negative shares issued) is the same as that indicated above. (In the case where only a few members have received anticipated earnings in excess of the proper amount (that is, greater than the proportion to which they are entitled), the shares should be issued (or deducted) on a pro rata basis. The excess anticipated distributions received by those members would be recorded as monetary debts to be paid out of interest or the future value of the shares on the date of cashing out; in reality we are talking about monetary debt here, and not changes in the ownership structure of the enterprise.14

6. Having examined the matter of issuance of new shares, we immediately confront the question of how to distribute the shares among the members. The application of a standard of strict equality (an equal number of shares to each member) would surely be unjust or unfair since the contributions made by each member will have been different. Cooperativism is known for the just and rational criterion of distribution based on patronage, that is, in proportion to the contributions made. In a worker cooperative, the practical application of this criterion should take into account the complexity of labor benefits and the system of ownership.15

As is normal, the hours worked by members over the course of a given fiscal year may differ. Moreover, the type of work done is qualitatively distinct in terms of the skill level of the labor power involved and the functions and services performed. The labor of a worker with little technical training, that of an administrator or a technical specialist, etc. have different values. That is, they contribute in different proportions to the creation of surplus for the enterprise.

Obviously, this needs to be recognized, as much in the monetary remuneration of labor as in the individual member’s right to ownership of the equity (labor shares). To do otherwise would amount to – once again – an unfair transfer of wealth, and would make it harder to recruit in necessary quantities specialist labor or labor with a larger technical or scientific element.

It is necessary, then, to elaborate a scale by which to weight the labor time of each member according to its degree of skill and productivity. How to do this, and the criteria to use in determining the factors involved in creating such a scale, as well as the discussion of the foundations and justification of this weighting, will be examined in the next chapter, when we examine the treatment of labor in cooperatives. For the moment it is sufficient clearly to establish the criterion that recognizes that, in the distribution of surplus, there are differences in productivity among workers.

In order to measure the contributions of “internal human factors” made by workers and calculate the corresponding allocation of profits, the aforementioned differences in worker productivity should be measured in units of simple labor, the same as for internal objective factors. We shall see in the next chapter that this is possible and even easy to do. For now, let us assume it to be true and see how the differential contributions of the workers can be taken into account when distributing surplus and “labor shares.”

Now, assuming we have properly grasped the meaning of equity and its measurement in an enterprise organized by Labor, we can add an additional line to the table in which we established the contributions of the workers to the objectified equity of the enterprise, specifying for each worker the weighted total of days of simple labor performed in the enterprise in the course of the fiscal year. Some will have worked more days during the year and some fewer, and the sum of days for each member will be multiplied by a factor corresponding to the weight assigned to the type of labor performed.

We will have then the exact statement of the contributions made to the enterprise over the year by each member, to which will correspond a proportional amount of compensation, that is, the share of the surplus that each merits. The contributions of internal factors made by each member in the case of the enterprise we have been considering are seen in the following table.

It is clear that the distribution of surplus and profits should not be made solely on the basis of each member’s direct labor contributions, but their total labor contributions. In effect, the surplus generated is not the result of their direct labor alone but also of the use of previous labor, which is to say, of objectified factors in the accumulated equity, which also have a specific productivity. Hence, the surplus corresponds to the combination of previous and current labor applied and put to use in the enterprise.

In a market economy, if the remuneration due to internal objectified factors (cooperative “capital”) is not recognized you will see a spontaneous movement among workers to withdraw their portion of the equity and place it in the external capital market, where it can earn a fixed rent or interest rate.

We will see later on that the accumulated equity in the enterprise belonging to each member can only be withdrawn when the worker leaves the enterprise – except in very unusual cases authorized by the workers as a group – but this restriction on the withdrawal of property does not by itself eliminate the problem. Nor does it resolve it theoretically, because the failure to remunerate the “capital” of the members will in any case constitute a disincentive for investment and discourage workers who are considering investing their own savings in the enterprise and in the cooperative sector. Moreover, once it reaches a certain volume, the member’s share of the equity placed on the market, outside of the enterprise, could earn interest rates greater than the remuneration that each member obtains for their work in the cooperative. In that case it would make more sense for the member to withdraw it from the enterprise and place it in an investment with a fixed rate of return, and, ultimately, seek employment somewhere else (perhaps even in another cooperative, thus avoiding the loss of the advantages of participatory and self-managed work). The enterprise from which the worker’s share of equity and their labor is withdrawn would be negatively affected and see its ability to recruit new worker members decline, as we shall soon see.

Recognizing the need for remuneration of member contributions to equity is not a concession that worker enterprises make as a result of operating in a market economy dominated by capitalist criteria; it simply corresponds to the specific logic of this type of enterprise and to the principles of distributive justice.

If it is appropriate for the organizing category of the enterprise – Labor – to remunerate all the factors that it hires and employs, including external financing obtained through loans and the land or material means of production it leases, why should the financial and material contributions of the worker-members, which consist of the accumulated unalienated labor of workers, not also be remunerated?

The objectified factors contributed by workers will not be remunerated at fixed market prices – as are the external factors, contracted on the market – but instead receive variable compensation according to the surplus produced in the current fiscal year. It is to this potentially more rewarding end that the workers have decided to risk their contributions in their own enterprise instead of putting them in another project.

One might suppose that in proceeding in this way we are introducing a principle of growing income inequality among the members of the enterprise. In reality something different happens: over time member incomes as well as the equity they hold in the enterprise come to approximate a distribution proportionate to the contributions they make in the form of direct labor. In this case, two possibilities emerge.

One is that members’ initial contributions (initial capital contribution and other financial and material contributions) may be of equal value or less differentiated than the contributions that are made in the form of direct labor. In this case, the combined remuneration of cooperative “capital” and direct labor have a leveling function with regard to total income per worker. In effect, if the initial contribution of objectified factors is equal (or nearly) without regard to skill level or training of labor power, the surplus distributed on the basis of contributions of objective factors will be equal for all (or nearly), and the differences in income between them will apply only to that part of the surplus which is distributed on the basis of direct labor. Combining the two criteria, the total allocation to the members of the worker enterprise will be, then, proportionately more equal than if the surplus were distributed solely on the basis of direct labor. Now, as the equity grows through the reinvestment of a portion of the surplus, one will see a progressive tendency toward proportionality in the resulting ownership structure based on the direct labor contributions of each member. The initial leveling effect will gradually diminish and the ownership structure will become more differentiated; but only to the point that the differences in equity equal the differences in productivity of the direct labor performed by each worker.

The other possible scenario is one in which the individual members make different initial contributions of objective factors resulting in an initial ownership structure that is more imbalanced than it would be based on direct labor contributions alone. Undoubtedly, these different contributions (which represent sacrifices that each member makes for the enterprise) will be differentially reflected in the income of each member, on top of differences resulting from the human factor contributions alone, which are integrated into the labor power of each member.16 So, the allocation of surplus based on the combined remuneration of both types of factors will lead, over time, to a progressively equalized structure of ownership and distribution of surplus, tending to correspond to the direct labor contributions made by each member to the enterprise. The reason is the same as in the previous case: the initial capital contributions (which correspond to previous labor) will play a diminishing role in the structure of member contributions of objective factors, while the wealth generated by the enterprise itself will become more important.

In synthesis, as soon as we recognize that there are different types and intensities of labor, and that workers should participate differently in the surplus of the enterprise on this basis, we see that the shares of ownership held by the members of the enterprise will never be equal. If all the members made constantly increasing contributions to the equity in absolute terms (leaving aside losses, which would lead to a process of disinvestment), the proportions in which the different members participate in ownership would slowly change: some would see their equity grow more than others. These changes would tend to lead to a convergence of members’ relative proportions of ownership with their different contributions of direct labor.

This ownership structure and system of surplus distribution does not lead to a process of “capitalist” concentration of ownership. In capitalist enterprises the differentiation in ownership encounters no structural limits. In workers enterprises, on the other hand, the accumulation of internal human factors, that is, accumulation in terms of personal growth (growth of members’ own capacity and potential which they contribute through their direct labor) sets structural limits to concentration of ownership.

Certainly, the differences among members can be fairly significant. Between the unskilled worker and the highly specialized expert one can see considerable differences in productivity. This is a fact of social, economic and cultural reality. It is interesting to observe, nonetheless, that precisely due to cooperation in work and management, which encourages worker interaction and integration, cooperative enterprises (worker and community cooperatives) are especially good at enabling and facilitating transfers of capacities and skills. These flows of human factors within the enterprise progressively reduce differences in degrees of personal development and levels of contributions made by the different associated workers. Thus we see that cooperativism and worker self-management tend toward growing equality, but do so while correctly recognizing differences in contributions.

7. Defined in this way, a system of ownership and distribution of surplus and gains that takes into account the contributions of both objective and human factors made by each individual raises the question: in what proportions should the two elements be remunerated? Although at these heights of analysis the answer is fairly obvious and does not cause us any problems, we should pose and examine if carefully; in the doctrine and practice of cooperativism this theme has always posed notable problems.

In the first version of this book we ran into this problem. Having examined the habitual procedures in cooperative practice, we analyzed it as a special problem and sought to apply in the best manner the criterion of pro rata or patronage distribution. Reconstructing this analysis today with more precise concepts, we find our earlier treatment insufficient. The analytical and practical usefulness of the initial analysis is unchanged: incorporating “units of simple labor” as a single criterion of measure for both types of factors permits us to resolve the problem in an exact way and with full coherence and autonomy of the cooperative method.

We said, at that point, that from the point of view of theory the criterion of pro rata distribution demanded that we remunerate both components in conformity with their respective productivity in the enterprise. We have not changed our view. But the problem is not one of criteria but of the way the criterion is applied. The productivity of “capital” and of labor can be mathematically determined only in a few cases, and in particular in enterprises whose production function (determined by its “capital”/labor ratio) is homogeneous – that is when the enterprise has constant returns to scale.17 This process of mathematical measurement, in addition to being inapplicable in many cases, gives rise to notable technical complexities. Thus, we suggested an alternative process that offers a good approximation: adopting the average or standard prices paid for “capital” and labor in the market as a criterion for establishing the proportions of surplus to assign to “capital” and to labor.

The proposed process would consist of calculating the rent that “capital” would obtain on the factor market, that is the “capital” of the workers enterprise, using as a reference the interest paid in the financial system for medium or long term use of funds and calculating the sum of the wages that would be obtained by labor power in the cooperative enterprise if the workers were wage laborers hired by a capitalist enterprise of similar size and technological make-up. Having established in this way a volume of rent and wages to be paid for an alternative use of the enterprise’s “capital” and labor power, the proportions in which the two factors are remunerated can be used to determine their respective shares of the surplus generated by the worker cooperative.

This way of resolving the question is better than the other more pragmatic ones that one could imagine and that have in fact been proposed, basically consisting of considering remuneration of one of the factors as a given and the other as a variable that depends on the amount of surplus generated. One such approach would consider the remuneration of the “capital” contributed or accumulated by the members as a fixed quantity, based on a market interest rate (which could be the interest paid on long or medium term investments); in that case the remuneration paid to “capital” would be deducted from the surplus and the remainder would be distributed pro rata based on the labor performed by each member in the period under consideration. Another way would involve considering the remuneration of direct labor performed as a fixed amount, using the criterion of average wages paid in the labor market; in that case the payments made to labor would be deducted from the surplus and the remainder would be distributed in proportion to the “capital” contribution made by each member.

Both approaches are possible to apply in practice but neither satisfies the demands of the specific logic of the workers enterprise.

In effect, in the first case, the remuneration of “capital” would take the form of rent and in the second the remuneration of labor would take the form of wages. In both cases, we are dealing with procedures derived from capitalist firms, which make possible – especially if the gains of the enterprise are high – the emergence of a process of concentration of “capital” that leads away from the distribution of ownership corresponding to the contribution of direct labor.

In the workers enterprise, the cooperative “capital,” as much as the direct labor, both contributed by members, are placed at risk so their remuneration should not be fixed but should depend on the gains made by the enterprise, due to the efficiency of its management. For this reason, the criterion for distributing surplus between “capital” and labor should define a proportion with respect to such surplus, a proportion that remains constant whatever its volume. The proposal that we made to recompense both factors on the criterion of the “alternative or opportunity rents” (as established by the factor markets) points precisely to this conclusion.

The only thing that this last process does not resolve completely is the dependent relation between the calculation of the “remuneration” of factors, with respect to the capitalist market (in which capital dominates as the organizing category), where it happens – as we warned – that the compensation for capital is often higher than it would be if it were remunerated according to its marginal productivity. The proportion in which factors are remunerated in the market would correspond to that which would be fair and exact in the cooperative enterprise only if the market were characterized by “perfect competition.”

This dependence disappears, without creating additional technical or accounting difficulties (on the contrary the calculation is simpler), once we reduce internal objectified labor and internal human labor to a homogeneous unit of measurement: units of simple labor. This unit of measurement, applied in the form we explained earlier shows us the exact proportions in which the surplus should be distributed among the members in accordance with their respective contributions of both types of factors. Taking the earlier example (Table 2), the distribution would be as follows:

Only one more element needs to be added in relation to distribution of surplus and it is the necessity of specifying – in order to avoid any confusion – that there is no reason for the portion of surplus distributed in remuneration of contributions of objectified factors to be equivalent to that part which is directed to productive investment (or accumulation of objectified factors), nor to the portion of surplus, based on direct labor, that is distributed in anticipation to meet the consumption needs of the workers. We are dealing with two moments and two distinct economic and accounting operations. With the criterion of combined remuneration of contributions of objectified factors and human factors (of “capital” and of direct labor) we determine the portion of surplus that corresponds to each member, summing the contributions each member made to both types of factors; this independently of whether they will receive this remuneration in money or in labor shares. On the other hand, the distribution of surplus in money and in labor shares is an operational decision made by the enterprise, taking into account the consumption needs of the workers and the investment needs of the enterprise, in a relatively independent manner from the quantities that correspond to each member.

Nonetheless, both operations of distribution are related in practice, because the remuneration of direct labor in money is performed mostly on a monthly basis, before the annual surplus is known, and is thus an anticipated distribution. Something similar happens with the process of investment in production, which is carried out on the basis of needs that present themselves in the enterprise at different times in the year and not always on the basis of predefined projects. In this way, a portion of surplus can turn out to be tied to distribution among the members in money or be assigned to them in shares without producing any distortion or maladjustment if the enterprise keeps adequate accounts, since any disequilibrium that occurs can be corrected a posteriori.

It is the workers themselves (members) who decide in what proportions the surplus distributed to them on the basis of their contributions will take the forms of money or labor shares. Now, it is necessary to take into consideration the fact that this decision is not given by the simple will of the associated workers who express their preferences in the assembly, since there is a series of economic relations and conditions that limit this sovereign will. In other words, the decision of the members is not arbitrary but must respond to the logic of efficient and rational functioning. We have already repeated it: the surplus generated by the enterprise does not materialize in its totality as available funds in the account but also consists of growth in physical assets, other immaterial assets, raw materials and accumulated supplies, funds for amortization, for education, debts to third parties, unsold inventory, etc. None of these values can be directly distributed among the members, instead, as they are elements of the process of accumulation, they must be distributed in the form of labor shares. Inversely, there are other conditions that require the distribution of other elements of surplus in the form of money: e.g., the monthly anticipated distributions to members are distributed in monetary form.

As for the mode of distribution of freely available funds (that part of the surplus that at the end of the fiscal year remains in the form of available money), not only the desires of the members but also the needs for expansion of the enterprise, as well as the market conjuncture, should be taken into account. In this sense it is very likely that a rapidly expanding enterprise will have more need for money in the short term than one with a relatively stable level of activity, and that implies that during an expansion process the distribution of money among the members will be temporarily low.

Let us suppose that the enterprise prospers and grows due to growing demand for its products; to respond to this demand the enterprise should first increase its spending, since it will face the need to buy greater quantities of raw materials and supplies, expand its machinery and physical plant, introduce new lines of production, update technological processes, create sales offices, contract out for professional services, etc. All of this signifies short term need for capital. If one wishes to seize the favorable moment in all its expansive possibilities, the enterprise should direct the greatest possible proportion of its surplus to the growth of “capital,” reducing to a minimum the distribution of liquid money among its worker members. The latter will voluntarily make this sacrifice – within certain limits – because the money directed to investment remains their property, creating moreover the possibility of greater future gains. (This would not happen in a cooperative of the traditional type in which the property is held “in common” without recognition of the right of member to recover proportionally their contributions, which translates into a defunding of the possibilities offered by a favorable economic conjuncture, that is, into economic inefficiency.)